Key Takeaways

- Licensed money lenders in Singapore are regulated under the Moneylenders Act, but intimidation, threats, or abusive behaviour is considered money lender harassment and is not permitted.

- Borrowers should distinguish between normal repayment reminders and harassment, which involves coercion, repeated threats, or invasion of privacy.

- Unlicensed money lenders in Singapore often use aggressive tactics, hidden fees, and informal communication channels, making them significantly riskier than licensed money lenders.

- If harassment occurs, borrowers should stay calm, preserve evidence, verify the lender’s licence, and submit a money lender report to the police or Registry of Moneylenders.

- Borrowers can reduce risk by choosing verified licensed money lenders, understanding repayment obligations, and avoiding overborrowing or unsafe options such as illegitimate private money lenders or illegal loan offers.

Borrowing from a licensed money lender in Singapore can be a practical way to legally access funds for short-term financial needs. That said, while licensed money lenders are regulated under Singapore’s Moneylenders Act and must follow strict money lender rules when issuing and collecting loans, borrowers should also understand their rights throughout the repayment process.

Just to put it out there, debt collection should never involve threats, intimidation, or abusive conduct. Whether the issue involves licensed money lender harassment, an aggressive debt collector, or an unlicensed money lender Singapore borrowers encounter online, it is important to recognise when lawful debt recovery crosses the line into harassment!

Knowing how to identify improper behaviour, when and where to seek help for money lender harassment, and how to lodge a money lender report can help protect both your finances and your peace of mind.

What Counts as Licensed Money Lender Harassment?

Not every reminder about a missed payment constitutes licensed money lender harassment. Licensed lenders are entitled to contact borrowers regarding outstanding repayments. However, there is a clear distinction between professional debt collection efforts and conduct that causes fear, distress, or intimidation.

Common Harassment Behaviours

Money lender harassment may take many forms. While licensed money lenders are allowed to communicate with borrowers about outstanding repayments, certain behaviours may cross the line into intimidation or abuse.

Examples of money lender harassment include:

- Repeated threatening or aggressive calls, texts, or messages

- Threats of violence, property damage, or public shaming

- Harassing family members, employers, colleagues, or neighbours

- Using abusive language or intimidation during repayment discussions

- Making unwanted visits to a borrower’s home or workplace in a threatening manner

- Sharing a borrower’s debt information with unrelated third parties

If you experience any of the above, it may be appropriate to document the incidents and consider filing a money lender report with the Registry of Moneylenders as soon as you can. Licensed money lender harassment should never be tolerated!

Lawful Repayment Reminders vs Harassment

Licensed money lenders may communicate with borrowers about payment obligations, especially if instalments have been repeatedly missed. However, these communications should remain professional, reasonable, and respectful.

Licensed money lender harassment begins when communication becomes excessive, threatening, coercive, or is designed to pressure borrowers through fear rather than lawful debt recovery procedures. Understanding this distinction can help borrowers determine whether a situation warrants a money lender report to the relevant authorities.

Licensed vs Unlicensed Money Lenders in Singapore

One of the best ways to avoid future problems is to understand the difference between legitimate lenders and illegal operators before accepting a loan.

How Licensed Money Lenders Operate

Licensed money lenders are regulated by Singapore’s Registry of Moneylenders and must comply with legal requirements governing loan issuance and debt collection. They are required to provide clear contracts outlining interest rates, fees, repayment schedules, and other key terms.

Borrowers should have a clear understanding of their obligations before signing any agreement. Legitimate lenders also follow proper identity verification and credit check procedures and operate from approved business premises.

A legitimate private money lender will never offer a fully remote loan process! Before taking out any loan, borrowers should always verify that the lender is on the official Registry of Moneylenders list.

Signs Singapore Borrowers Should Avoid

Many complaints involving money lender harassment originate from illegal lending operations rather than legitimate lenders. An unlicensed money lender that Singapore residents encounter may approach potential borrowers through unsolicited messages or advertisements.

Warning signs of a potentially illegal private money lender include:

- Unsolicited loan offers via WhatsApp, SMS, Telegram, or social media

- Requests for Singpass credentials, ATM cards, banking passwords, or other sensitive information

- Demands for upfront fees before loan approval or disbursement

- No formal loan contract or unclear borrowing terms

- Refusal to meet at a registered business address

- Aggressive or threatening behaviour before or after the loan is issued

These practices are commonly associated with illegal lending activities and should be treated as serious red flags.

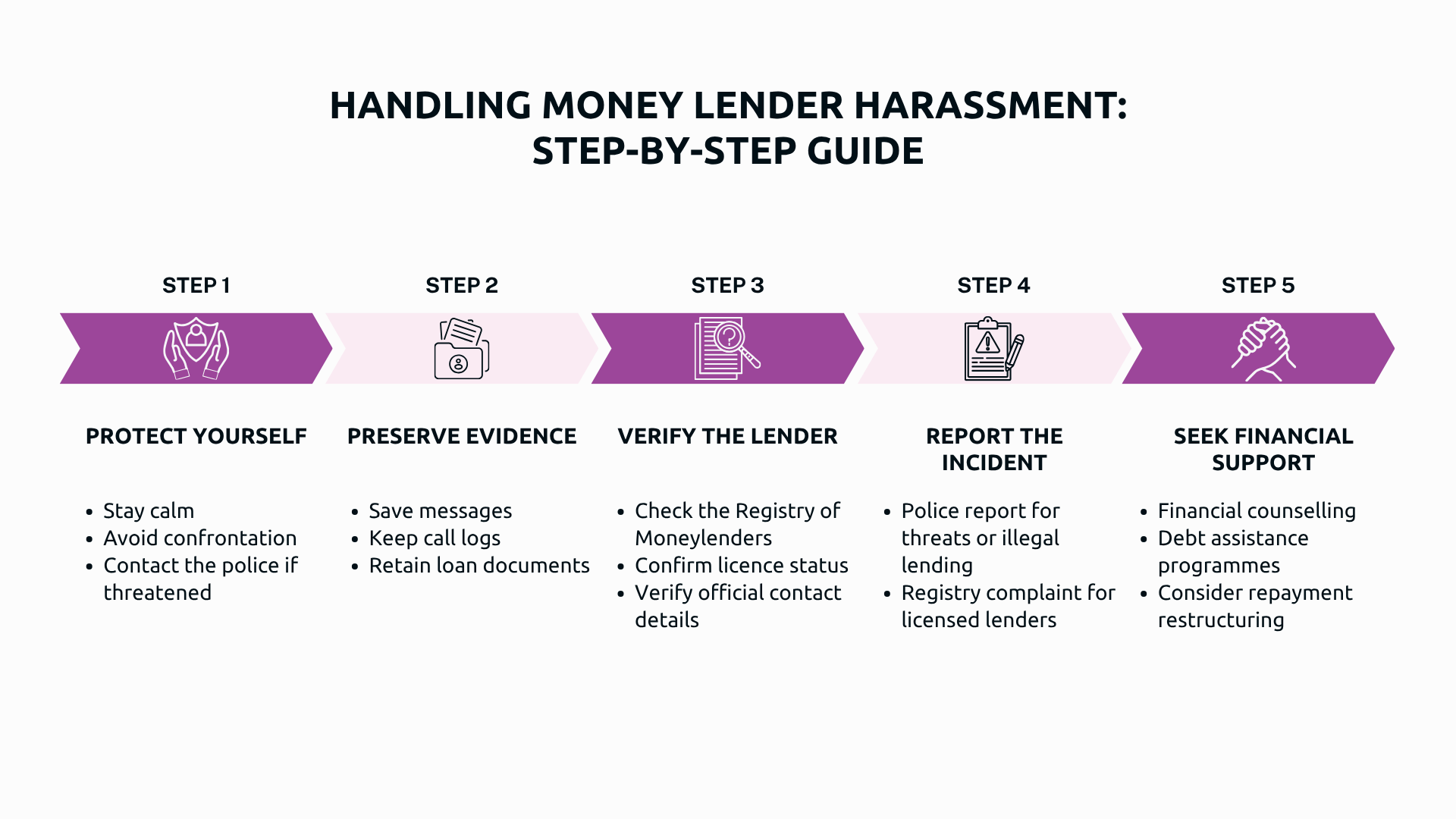

What to Do if You Experience Money Lender Harassment

Experiencing harassment can be stressful, but taking the right steps early can help protect your rights and support any future investigation.

Reporting Money Lender Harassment in Singapore

Knowing how to submit a money lender report can help ensure that complaints are directed to the appropriate authorities.

Information You Should Prepare

Before submitting a money lender report, gather as much supporting information as possible.

Useful information includes:

- The lender’s or the loan company’s name and licence number

- Contact numbers and communication channels used

- Websites, social media profiles, or messaging accounts involved

- Loan agreements and repayment records

- Screenshots or evidence of threats, harassment, or intimidation

- Police report reference number, if one has already been filed

Having these details ready can help streamline the reporting process and support any subsequent investigation.

Where to Submit a Report

The appropriate reporting channel depends on the nature of the issue. Threats, intimidation, violence, vandalism, or suspected loan shark activity should be reported directly to the police.

Complaints involving licensed money lenders may also be submitted to the Registry of Moneylenders for review.

What Happens After You Report

Once a money lender report has been submitted, authorities may assess the information provided, request additional documentation, investigate the matter, and take appropriate enforcement action where necessary.

The timeline varies depending on the complexity of the case and the evidence available. Cooperating fully and maintaining organised records can help support the process.

How to Avoid Money Lender Harassment Before Borrowing

Prevention is often the best form of protection. Taking a few precautionary steps before borrowing can significantly reduce the risk of future disputes.

Borrow Only From Verified Licensed Money Lenders

Always verify a lender’s licence status before applying for a loan. Visit the registered business address, where possible and ensure that all terms are properly documented before signing any agreement.

Understand the Full Cost of Borrowing

Borrowers should review interest rates, administrative fees, and late payment charges carefully. Be cautious of lenders promising guaranteed approval or instant cash without proper checks, as these claims are often associated with questionable lending practices.

Borrow Within Your Repayment Ability

Many borrowers ask, “How much can I borrow from money lender services in Singapore?” While borrowing limits depend on factors such as income and loan type, the more important consideration is how much you can comfortably repay!

Borrowing beyond your means can create unnecessary financial pressure and increase the likelihood of repayment difficulties later on. Always be prudent!

Why Choosing a Reputable Licensed Money Lender Matters

Not all private money lenders operate with the same level of professionalism and transparency. Choosing a reputable licensed lender can make a significant difference to your borrowing experience.

At Synergy Credit, borrowers are guided through the loan process with clear explanations of interest rates, repayment schedules, fees, and obligations before any agreement is signed. Transparent communication helps borrowers make informed decisions and reduces the risk of misunderstandings throughout the loan term.

That’s not all. Working with a regulated lender also provides greater confidence that all lending and collection activities are conducted within Singapore’s legal framework.

Conclusion

Licensed money lender harassment should never be ignored. While licensed money lenders are permitted to collect legitimate debts, harassment, intimidation, and abusive collection practices are unacceptable.

If you experience money lender harassment, remain calm, preserve all evidence, verify the lender’s licence status, and submit a money lender report to the relevant authorities when necessary. Seeking financial assistance early can also help prevent repayment difficulties from becoming more serious problems.

Most importantly, protect yourself by borrowing only from verified and reputable lenders. If you are considering a loan and would like transparent, obligation-free guidance on your options, speak with us to better understand your borrowing choices before making a decision.

Frequently Asked Questions

Can a licensed money lender visit my home or workplace?

A licensed lender may attempt to contact borrowers regarding repayment matters at their home or workplace. However, threatening, intimidating, or disruptive behaviour is not permitted and should be reported if it occurs.

Can a money lender contact my employer or family?

Disclosing a borrower’s debt information to unrelated third parties may be considered inappropriate and could potentially form part of a complaint, depending on the circumstances.

What should I do if a debt collector is harassing me?

Debt collectors are also expected to operate within legal boundaries. If a debt collector engages in threats, intimidation, or other improper conduct, you should document the behaviour and report it to the appropriate authorities.

Can I report an unlicensed money lender?

Yes. If you suspect you are dealing with an illegal lender, particularly one making threats or engaging in intimidation, you should report the matter to the police immediately.

Can I make a report anonymously?

Some reporting channels may allow anonymous submissions. However, providing your details and supporting evidence generally improves the authorities’ ability to investigate the complaint effectively.